The core of the DCF model involves three key components:

Forecasting Cash Flows: This is where you project the company’s expected cash flows over a certain period, typically 5 to 10 years. These projections should include all cash inflows and outflows that are expected to occur.

Selecting a Discount Rate: This rate is crucial as it will be used to ‘discount’ the future cash flows back to their present value. This rate typically reflects the cost of capital or the risk-free rate plus a risk premium.

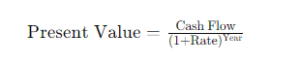

Calculating Present Value: Using the discount rate, the future cash flows are discounted back to the present day, which provides a value that represents the total value of the company.

Example of DCF in Action

Let’s consider a hypothetical company, Tech Innovations Inc., which is looking to expand its operations. Analysts predict that the company will generate the following cash flows over the next five years:

- Year 1: $150,000

- Year 2: $180,000

- Year 3: $210,000

- Year 4: $240,000

- Year 5: $270,000

Assuming a discount rate of 10%, let’s calculate the present value of these cash flows.

Calculation:

- Year 1 PV = $150,000 / (1.1)^1 = $136,363

- Year 2 PV = $180,000 / (1.1)^2 = $148,760

- Year 3 PV = $210,000 / (1.1)^3 = $158,110

- Year 4 PV = $240,000 / (1.1)^4 = $165,289

- Year 5 PV = $270,000 / (1.1)^5 = $170,576

The total present value of these cash flows is $779,098.